Deal Abstract

https://republic.co/elemeno-health

Education platform providing just-in-time reference and tips to healthcare professionals. Backed by Y-Combinator, $900k in revenue to date. Burn is $120k and raised 8 months of runway to try and 2x revenue and clients by Q2 2021.

Shoutout to A.S. for the tip!

Decision

Pass.

Why Investing/Passing

- Valuation Too High/Company Too Mature: I’m looking for companies sub-$10 million valuation.

- Health Tech Not My Jam: I’m not bullish on medical organizations being motivated to adopt the newest, most efficient technology at a very rapid pace. That said, maybe COVID changes the equation.

- Seems More a Sales Play than a Technology Play: Solid business but uncertain it’s venture backable.

The 6 Calacanis Characteristics (91 161 18)

| Check | Yes/No |

| 1. A startup that is based in SV | Yes: Oakland, CA |

| 2. Has at least 2 founders | Yes: 2 |

| 3. Has product in the market | Yes |

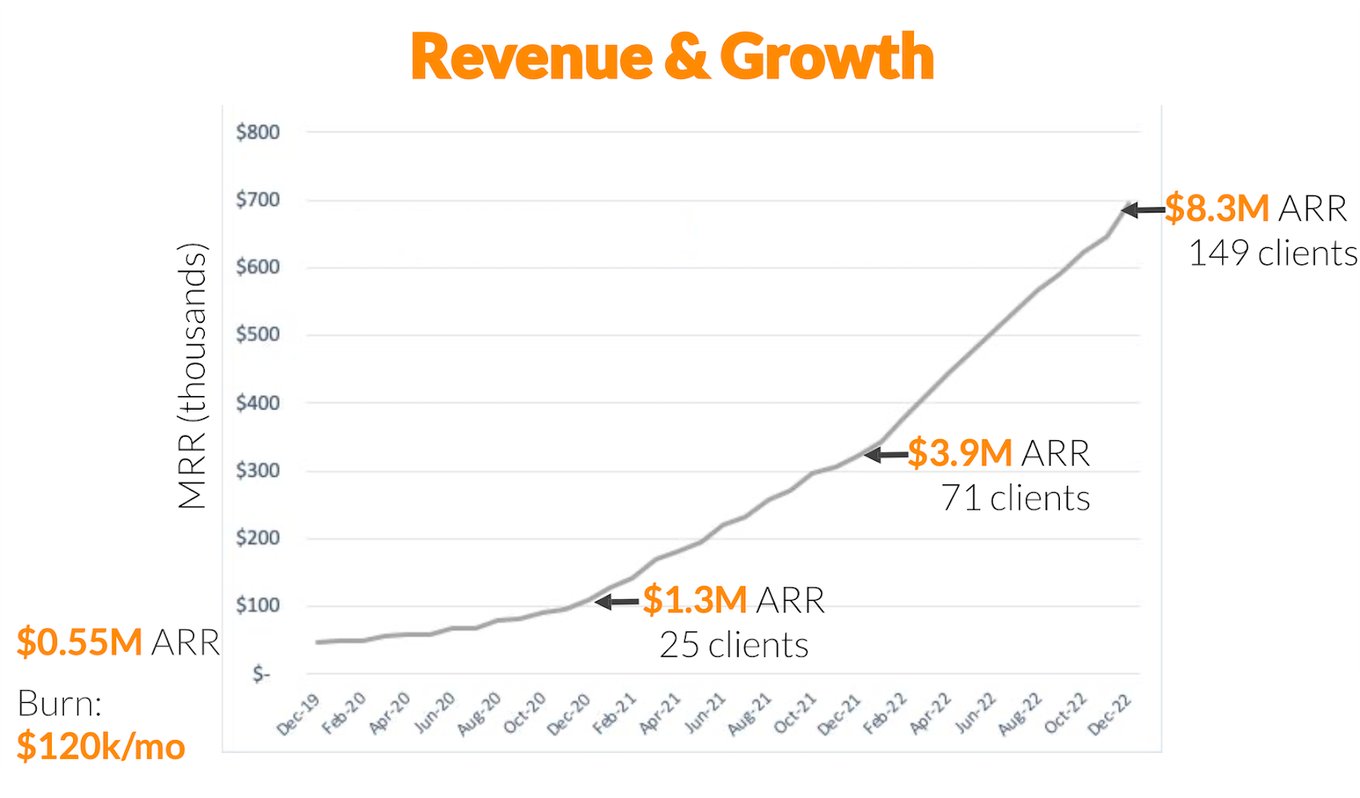

| 4. 6 months of continuous user growth or 6 months of revenue. | Yes: See revenue and growth chart from team. |

| 5. Notable investors? | Yes: Y-Combinator |

| 6. Post-funding, will have 18 months of runway | No: Burn is $120k/mth, fundraised $1,070k which is 8-9 months. |

The 7 Thiel Questions (ETMPDDS)

- The Engineering question:

- Uncertain: Not sure their EdTech solution is that much better than existing technology. That said, they can sell..

- The Timing question:

- Fine: COVID and the like.

- The monopoly question:

- Good: Could scale quickly, impressive stats about time to deployment.

- The people question:

- Good: CEO and CTO are strong.

- The distribution question:

- Good: Selling to hospitals is hard, and the CEO is a former medical director.

- The durability question:

- Good: selling to hospitals is hard but very defensible.

- *What is the hopeful secret?:

- Charging money for a hospital edtech solution is a large, scalable business.

What has to go right for the startup to return money on investment:

- 100x Revenue: In April 2020, valuations for SaaS companies was ‘the median public SaaS company valuation multiple stands at 8.2 times ARR.‘ In other words, for a company to be worth $1 billion, it must have around $100 million in annual recurring revenue. Zoom achieved $100 million in ARR and unicorn status in 2017.

- Go from Founder Centric Sales to Sales-Team Focused: Having 10+ hospital partners across the US is good, but probably focused on the founder’s relationship and background. This is a great/critical way to start, but scaling beyond this will be essential for hitting that revenue number.

- Attribution of Value Creation: What will it take to get every medical professional lobbying their department head to buy this product? How much credit can Elemeno take for reducing stress and burnout, medical errors, and waste.

What the Risks Are

- Success Has Been Contingent on Founder/Not the Product: If the company’s unique defensible advantage is

- Painkiller, Not Vitamin: Intimately tied to attribution of value creation. The mental and cognitive biases of doctors and healthcare professionals is a popular research topic.

- Adoption Lag in Healthcare: I don’t think of healthcare organizations as early movers on new technologies.

Muhan’s Bonus Notes

Writing this deal memo was the first time I explicitly realized and articulated the search for billion dollar companies is searching for categories of startups with certain revenue potentials:

- For SaaS: $100MM ARR assuming a 10x multiple (e.g. Zoom, Calm)

- For Marketplaces: $300MM AR assuming a 3.7x multiple (the recurring revenue makes a big difference, TripAdvisor, Yelp)

- Consumer Internet

- E-Commerce

- Hardware: I prefer not to touch.

If we want to choose on a number for convenience, startup investors should look for companies that can grow to $250MM in 5-10 years. To put that into startling context, if you take a company with $100k ARR in year 0, it has to grow at ~2.2x continuously compounded for a decade to reach that type of growth. Great resource about Bessemer about valuations. Related. This would be weekly growth rate of 1.5%. Putting this into context with Paul Graham’s needs for YC companies, the need for 5-7% weekly growth at the beginning makes complete sense, especially anticipating the hitting of the plateaus of S curves.

Financials (References)

- Current Fundraised: $1.07M

- Valuation: 18MM

Updates

This is where I’ll post updates about the company. This way all my notes from offering to post-offering updates will be on one page. Also, somewhat of a dearth of materials (whose the team? where are the comments? why are the financials so opaque?)